Dual-cell LCD Market Size by Technology (IPS, VA, OLED, and Others), and by Application (Smartphones, Televisions, Monitors, Laptops, Tablets, Automotives and Others)- Global Opportunity Analysis and Industry Forecast 2024-2030

Market Definition

The Dual-cell LCD Market was valued at USD 745.5 million in 2023 and is predicted to reach USD 2044.2 million by 2030 with a CAGR of 15.5% from 2024 to 2030.

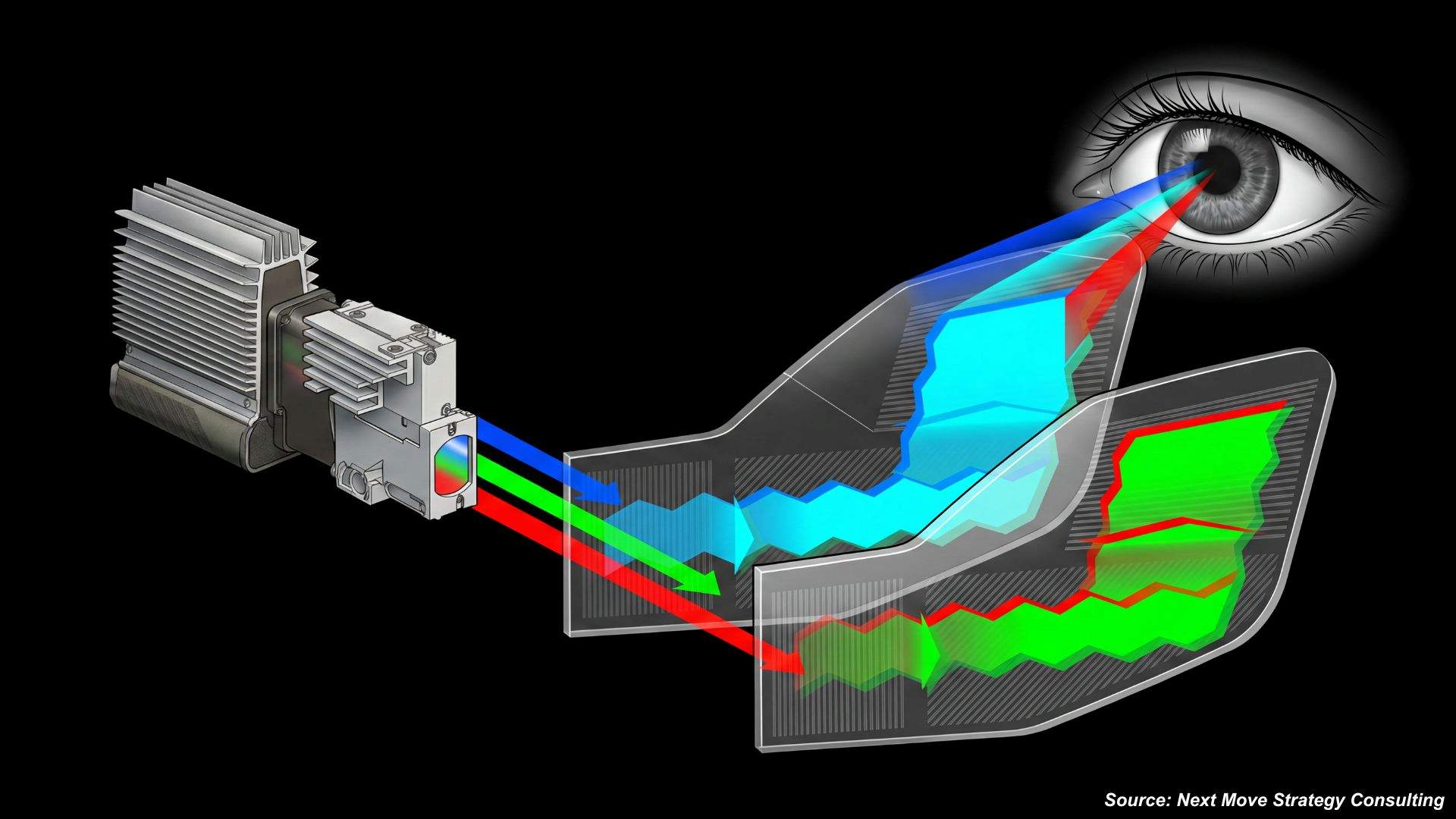

Dual-cell LCD is a display technology used in LCD (liquid crystal display) screens that involves the use of two layers of liquid crystal cells to enhance the display's contrast and color accuracy. In a dual-cell LCD screen, the front layer contains smaller cells, which are used for displaying dark and shadow areas, while the back layer contains larger cells, which are used for displaying brighter areas. The two layers work together to create a more detailed and vivid image, with improved contrast and color accuracy. The use of dual-cell technology in LCD screens has several advantages over traditional LCD displays. It can produce deeper blacks and brighter whites, resulting in a higher contrast ratio, and it can display a wider range of colors with greater accuracy.

Market Dynamics and Trends

The demand for smart materials is gaining traction due to the rising demand for high-quality displays. The demand for high-quality displays with excellent image quality, color accuracy, and contrast ratio has increased rapidly in recent years. Dual-cell LCD technology offers superior contrast ratios and color accuracy, making it an attractive choice for high-end display applications.

Moreover, dual-cell LCD displays are also gaining popularity in the automotive industry, where they are being used in dashboard displays, infotainment systems, and other applications, thus it is further boosting the growth of the market. This is due to their ability to provide better image quality and contrast ratio in bright sunlight, making them ideal for outdoor displays. According to the International Energy Agency, electric vehicle (EV) sales are projected to maintain robust growth through 2023.

In the first quarter alone, over 2.3 million electric cars were sold, marking a 25% increase compared to the same period last year. By the end of 2023, sales are expected to reach 14 million, reflecting a 35% year-on-year rise, with new purchases anticipated to accelerate notably in the second half of the year.

Furthermore, the rising demand for energy-efficient displays are fuelling the growth of the dual-cell LCD display market. Dual-cell LCD displays can offer improved energy efficiency compared to traditional LCD displays, as they can block more light from the backlight system, reducing power consumption. This is an attractive feature for manufacturers looking to reduce the energy consumption of their products.

However, dual-cell LCD displays are more expensive to manufacture compared to traditional LCD displays, thus it may restrain the growth of the market. This is due to the extra layer of cells required to produce the enhanced contrast ratio and better image quality. On the other hand, the introduction of new technologies such as mini-LED backlighting and quantum dot technology are expected to create ample growth opportunities for the market in the future.

Market Segmentation and Scope of Study

The global dual-cell display market is segmented on the basis of technology, application, and region. Based on technology, the market is classified into IPS, VA, OLED, and others. Based on the application, the market is segmented into smartphones, televisions, monitors, laptops, tablets, automotives, and others. Regional breakdown and analysis of each of the aforesaid classifications include regions comprising North America, Europe, Asia-Pacific, and RoW.

Geographical Analysis

Asia Pacific dominated the global dual-cell LCD display market and is potently expected to remain dominant in the market throughout the forecast period. This is attributed to the growing demand for smartphones in countries such as China and Japan, which are major markets for dual-cell LCD displays. Dual-cell LCD displays are becoming increasingly popular in the smartphone industry due to their ability to improve image quality and reduce power consumption.

According to the China Academy of Information and Communications Technology (CAICT), the total consignment of 5G mobile phones in China was 266 million units in 2021, which is 75.9% of total mobile phone shipments and a year-on-year increase of 63.5%. Moreover, the rapid adoption of cellular IoT technology in countries such as China is driving the demand for dual-cell LCD displays in the Asia Pacific region.

With China leading the way by recording 1.84 billion cellular IoT connections in 2022, according to the Ministry of Industry and Information Technology (MIIT), there is a growing need for advanced display technologies to support the increasing number of IoT-enabled devices. As more devices incorporate dual-cell LCD displays to enhance visual performance and efficiency, the market for such displays in Asia Pacific is experiencing significant growth driven by the expanding IoT ecosystem.

North America is projected to exhibit substantial growth in the global dual-cell LCD display market owing to the rising online gaming industry in the region. According to the American Gaming Association (AGA), commercial gaming revenue reached USD 60.42 billion in 2022, which is a 13.9 percent increase over 2021 and 38.5 percent higher than 2019. Gamers demand high-quality displays with fast response times and high refresh rates, and dual-cell LCD displays can meet these requirements. As a result, manufacturers are increasingly targeting gamers with their dual-cell LCD displays, which in turn is driving the market.

Moreover, the rising adoption of electric vehicle in the region is further boosting the growth of dual-cell display market. According to the International Energy Agency, electric car sales in the United States increased 55% in 2022, reaching a global sales share of 8%.

As more automotive manufacturers introduce electric vehicle models, there is a growing need for advanced display technologies to enhance the driving experience and provide innovative features. Dual-cell displays offer improved visual clarity, contrast, and energy efficiency, making them ideal for use in the dashboards and infotainment systems of electric vehicles. With consumers seeking enhanced digital experiences in their vehicles, the demand for dual-cell displays is experiencing a significant boost in the North American market, fueled by the rising popularity of electric vehicles.

Competitive Landscape

The dual-cell LCD display market includes several market players such as Samsung Display Co., Ltd., LG Display Co., Ltd., AU Optronics Corp., BOE Technology Group Co., Ltd., Japan Display Inc., Sharp Corporation, Innolux Corporation, Tianma Microelectronics Co., Ltd., HannStar Display Corporation, CSOT (China Star Optoelectronics Technology) among others. These market players are adopting various strategies such as innovation and collaboration to maintain their dominance in the global dual-cell LCD display market.

For instance, in February 2023, Samsung launches new dual UHD curved display for gamers. The gaming monitor delivers 7,680×2,160 resolution and a 32:9 aspect ratio in one screen for the first time.

Also, in April 2021, AU Optronics Corp. launched new eyecare displays with exclusive built-in a.r.t. technology to protect eyesight for professionals. The display featuring non-reflective surface, anti-glare and anti-reflection creates reading quality and exquisite image quality superior to paper.

Key Benefits

-

The report provides quantitative analysis and estimations of dual-cell LCD display market from 2024 to 2030, which assists in identifying the prevailing market opportunities.

-

The study comprises a deep dive analysis of the dual-cell LCD display market including the current and future trends to depict prevalent investment pockets in the market.

-

Information related to key drivers, restraints, and opportunities and their impact on the dual-cell LCD display market is provided in the report.

-

Competitive analysis of the players, along with their market share is provided in the report.

-

SWOT analysis and Porters Five Forces model is elaborated in the study.

-

Value chain analysis in the market study provides a clear picture of roles of stakeholders.

Key Market Segments

By Technology

-

IPS

-

VA

-

OLED

-

Others

By Application

-

Smartphones

-

Televisions

-

Monitors

-

Laptops

-

Tablets

-

Automotives

-

Others

By Region

-

North America

-

The U.S.

-

Canada

-

Mexico

-

-

Europe

-

The UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Netherlands

-

Finland

-

Sweden

-

Norway

-

Russia

-

Rest of Europe

-

-

Asia Pacific

-

China

-

Japan

-

India

-

South Korea

-

Australia

-

Indonesia

-

Singapore

-

Taiwan

-

Thailand

-

Rest of Asia Pacific

-

-

RoW

-

Latin America

-

Middle East

-

Africa

-

REPORT SCOPE AND SEGMENTATION:

|

Parameters |

Details |

|

Market Size in 2023 |

USD 745.5 Million |

|

Revenue Forecast in 2030 |

USD 2044.2 Million |

|

Growth Rate |

CAGR of 15.5% from 2024 to 2030 |

|

Analysis Period |

2023–2030 |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

Market Size Estimation |

Million (USD) |

|

Growth Factors |

|

|

Countries Covered |

28 |

|

Companies Profiled |

10 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 working hours of analysts) after purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

KEY PLAYERS

-

Samsung Display Co., Ltd.

-

LG Display Co., Ltd.

-

AU Optronics Corp.

-

BOE Technology Group Co., Ltd.

-

Japan Display Inc.

-

Sharp Corporation

-

Innolux Corporation

-

Tianma Microelectronics Co., Ltd.

-

HannStar Display Corporation

-

CSOT (China Star Optoelectronics Technology)

")

About the Author

Sikha Haritwal is an assistant manager with strong expertise in market research, data analysis, and cross-functional coordination. She plays a key role in leading complex research initiatives, strengthening analytical rigor, and enabling data-driven decision-making across teams. Known for her leadership mindset and structured problem-solving approach, she supports process improvement, enhances operational efficiency, and contributes to building scalable frameworks that drive long-term strategic outcomes and organizational effectiveness.

Sikha Haritwal is an assistant manager with strong expertise in market research, data analysis, and cross-functional coordination. She plays a key role in leading complex research initiatives, strengthening analytical rigor, and enabling data-driven decision-making across teams. Known for her leadership mindset and structured problem-solving approach, she supports process improvement, enhances operational efficiency, and contributes to building scalable frameworks that drive long-term strategic outcomes and organizational effectiveness.

About the Reviewer

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

Supradip Baul is an accomplished business consultant and strategist with over a decade of rich experience in market intelligence, strategy, technology, and business transformation. His work has included rigorous qualitative and quantitative analysis across multiple industries, helping clients shape investment decisions and long-term roadmaps. Earlier in his career, he was associated with Gartner, where he contributed to industry-leading reports and market share analyses. He has worked with leading global companies and holds an MBA with a dual specialization in Marketing and Finance.

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Speak to Our Analyst

Speak to Our Analyst