Insurance TPA Market by Service by Type (Health Insurance, Property and Casualty Insurance, Workers' Compensation Insurance, Disability Insurance, Travel Insurance, and Others), by Services (Claims Management and Risk Control Management), and End User (Healthcare, Construction, Real Estate and Hospitality, Transportation, Staffing, and Other End User) – Global Opportunity Analysis and Industry Forecast 2024–2030

Industry: BFSI | Publish Date: 26-Apr-2024 | No of Pages: 306 | No. of Tables: 302 | No. of Figures: 202 | Format: PDF | Report Code : N/A

Speak to Our Analyst

Speak to Our Analyst

Market Overview

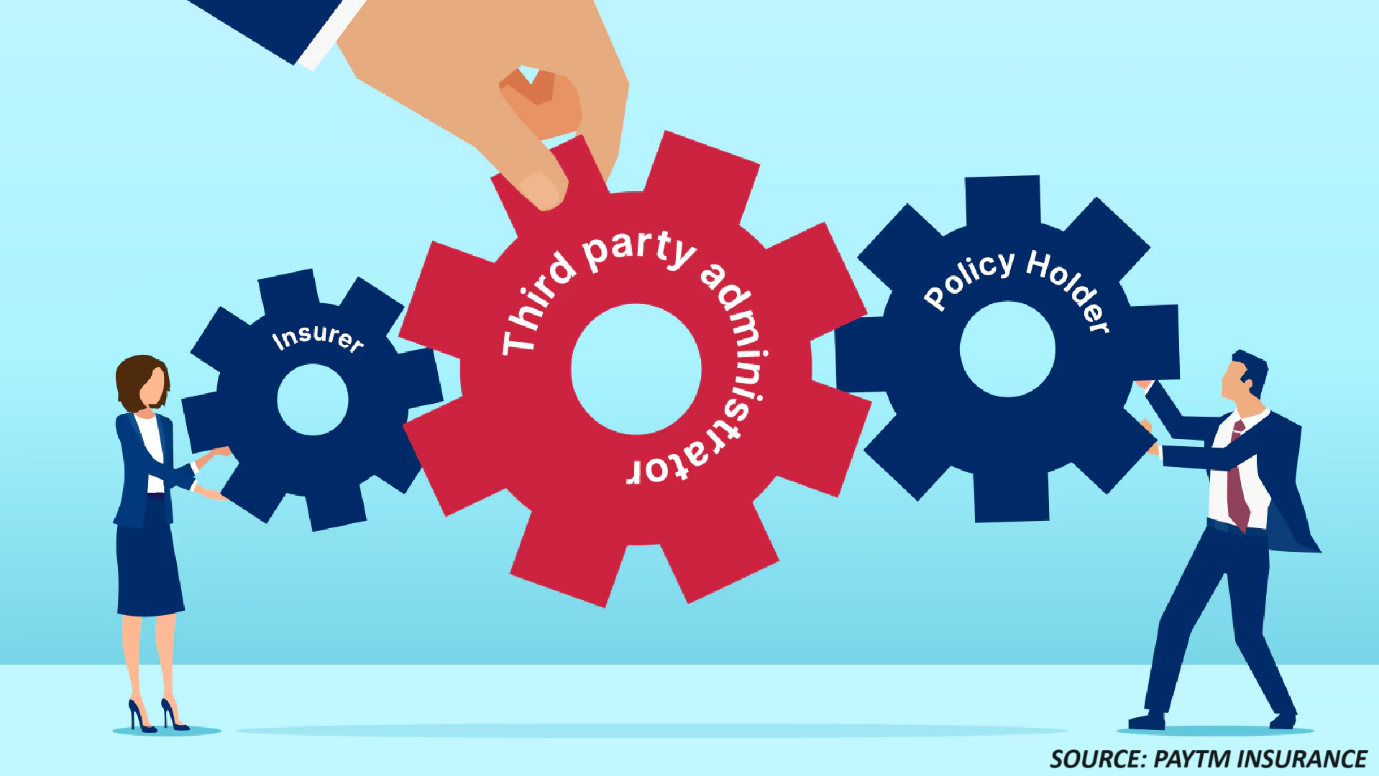

Insurance TPA Market was valued at USD 350.89 billion in 2023 and is projected to reach USD 535.22 billion by 2030 at a CAGR of 4.6% from 2024–2030. A third-party administrator (TPA) in the insurance sector that provides administrative services for insurance plans. These TPAs process insurance claims and manage specific aspects of insurance policies on behalf of insurers. Generally engaged by insurance companies, TPAs undertake various administrative responsibilities including claims processing, policy management, premium collection, and customer support. Serving as intermediaries between insurers, policyholders, and healthcare providers, TPAs facilitate seamless operations within the insurance industry.

TPAs play a vital role in the insurance sector by delivering specialized services that assist insurers in streamlining operations, enhancing efficiency, and cutting costs. They handle the day-to-day administrative functions related to insurance policies, enabling insurers to concentrate on risk underwriting and business expansion. The increasing demand for insurance is opening up new avenues for insurance TPAs. As it helps to play a pivotal role in assisting both companies and individuals in securing necessary insurance coverage while optimizing their premiums. Their ability to offer personalized services sets them apart from traditional insurance providers. With the escalating demand for insurance, the insurance TPA sector is poised for significant expansion. TPAs are strategically positioned to leverage this growth and emerge as integral players in the insurance landscape.

Rising Healthcare Expenses Accelerate the Demand for TPA

The need for third-party administrators is anticipated to increase due to the rising expense of healthcare. The expense of healthcare has experienced a boom over the past few years, and this growth is anticipated to continue due to the rise in chronic diseases such as cancer, diabetes, and heart diseases.

By reducing costs without compromising the quality of employee healthcare, TPAs have established themselves as a vital asset to self-insuring programs. As per the OECD Health Statistics 2023, the annual real growth in per capita health expenditure of OCED countries in 2021 was recorded at 8.1%, which is an increase of 88.4% from 2020.

In addition to extending lives and improving health, medical advancements raise spending and encourage excessive use of expensive technologies. This contributes to prompts both patients and physicians to demand the most advanced & expensive treatments and technologies available.

This increases the cost of treatment of diseases. Thus, investors are now paying attention to TPAs that provide efficient management of claims and offer transparency in the insurance process which accelerates the growth of the insurance third party administrator market.

Emerging Startups That Are Reshaping the Landscape of Operations in the TPA Industry

In the TPA sector, numerous startups are emerging that are redefining the traditional TPA business model by placing greater emphasis on streamlining processes through automation and faster claims handling.

Additionally, they prioritize providing transparent and reliable customer service to achieve satisfaction, comprehensive care, and efficiency. These companies offer a user-friendly interface and tailored benefit management, placing them at the forefront of the rapidly evolving TPA industry. It included companies, such as Flume Health Inc., Maestro Health, Empyrean, and others.

As an example, in 2023, Yuzu Health announced to disrupts insurance with affordable health plans for small businesses while using AI, as it simplifies claims processing and offers traditional and newer models such as reference-based pricing. The company recently secured USD 5 million seed funding and aims to expand and improve its tech. Yuzu Health targets small businesses needing better health insurance options, aiming to streamline claims and provide flexible, affordable coverage.

These startups have adopted a radically distinct approach to employer health plans. With the growing demand for innovative health technologies, startups worldwide are exploring unconventional methods to make healthcare more efficient, effective, and affordable. Some are facilitating connections between patients and local healthcare providers, while others are emphasizing preemptive care.

Many are also reimagining how patients purchase and pay for healthcare. Despite their differing approaches to efficient and effective healthcare, these companies share a common focus on patient-centric care and benefit advisory services. It includes companies, including ICHRA (Flyte HCM), SimplePay Health, Sana, and others.

Concerns Related to Cybercrime are Likely to Hinder the Industry

In the market, numerous insurers engage in competition and often depend on TPAs and external suppliers to ensure the seamless functioning of their operations. Consequently, TPAs are entrusted with the management of various administrative tasks for the organization.

Their responsibilities include acquiring and safeguarding confidential participant data, as well as ensuring the timely distribution of rewards. According to the most recent IBM Security data breach report, the global average cost of a data breach in 2023 stands at USD 4.45 million, representing a 15% increase over the past three years.

The market for insurance TPAs faces a significant constraint due to concerns surrounding security and privacy raised by external entities. Additionally, TPAs are primarily threatened by cybercrime, which has negatively impacted their reputation through unauthorized access to client information.

Lack of Technological Adoption by Traditional Players Limits the Industry Growth

Despite the availability of software capable of automating many administrative tasks, traditional TPAs still heavily rely on manual operations. This approach often involves time-consuming email correspondences, Excel spreadsheets, and lengthy phone calls, particularly during the claims process.

The efficiency of claims processing is further compromised by employees' limited expertise or experience in promptly and accurately documenting information, leading to common mistakes such as incorrect paperwork, wrong form submissions, lost documents, or delays in gathering materials. These inefficiencies hinder the claims process and contribute to its overall complexity.

Integration of Emerging Technologies Creates Opportunity for TPA Industry

The influence of technology on our lifestyles and industries is profound, driving evolution and impacting individuals and businesses alike. Technological advancements across various sectors have heightened competition within the insurance industry, enabling companies to expand their reach and enhance underwriting processes through data-driven insights. This technological progress also empowers TPAs to streamline claims handling and other operations, resulting in improved insurance services, enhanced customer experiences, and decreased operational costs.

Recently, Codoxo launched ClaimPilot, an AI tool automating healthcare claim audits. It targets professional claims, aiming to boost audit speed and clinician reviews while removing dollar thresholds. ClaimPilot will integrate with Codoxo's AI suite, covering the entire payment integrity process. This launch aligns with the growing belief in AI's transformative power in healthcare insurance claims.

The growth of the insurance TPA market is poised for substantial advancement with the integration of technologies such as wearables, blockchain, and artificial intelligence (AI). Wearable devices provide insurers with real-time health data from policyholders, enabling personalized insurance offerings based on individual health and activity levels.

By leveraging technology to optimize claims management and operations, TPAs can deliver efficient services, exceptional customer care, and cost savings, presenting lucrative growth prospects for key players in the insurance TPA market moving forward.

North America Market Holds the Dominant Share in Insurance TPA Market

The growing incidence of chronic diseases, including cancer, heart disease, and diabetes, can be traced back to unhealthy habits such as smoking, alcohol consumption, and poor diet. This trend has led to a surge in the demand for insurance policies, compelling insurance companies to engage insurance TPAs for effective claims management and processing in this area. The objective is to optimize operational efficiency and enhance service delivery in response to the increasing demand for insurance coverage.

According to the McKinsey & Company, there is an increasing burden of chronic disease globally, conditions including cardiovascular disease, cancer, diabetes, and respiratory ailments were responsible for 79% of deaths by 2020. Projections suggest that by 2030, this percentage could potentially escalate to 84%, underscoring the escalating impact of chronic diseases on global health outcomes.

Moreover, the region frequently experiences natural disasters, causing damage to homes, properties, and infrastructure. To improve the living conditions of residents in high-risk areas and alleviate the financial burden of disasters, communities and governments are collaborating to develop strategies and adapt to the effects of climate change, thereby safeguarding the region's infrastructure and ensuring the well-being of its inhabitants.

During 2022, the U.S. encountered 18 climate-related disasters exceeding USD 1 billion in damages. These events collectively incurred USD 175.2 billion in losses and tragically led to 474 fatalities. As a result, the surge in insurance claims stemming from these disasters is propelling the market expansion of insurance TPAs.

In addition, the robust presence of leading industry players such as Sedgwick Claims Management Services Inc., Gallagher Bassett Services Inc., Crawford & Company, and CorVel Corporation significantly bolsters the insurance TPA market in the region. These key players are expected to fuel market expansion through strategic initiatives such as product introductions and acquisitions, reinforcing their market dominance and leadership within the insurance TPA sector.

For instance, in April 2022, Gallagher Bassett International Ltd. (GB) acquired Claims Settlement Agencies Ltd. (CSA) to broaden its service offerings and expertise, ultimately enhancing the value delivered to both new and existing clients. This strategic acquisition also presents GB with the opportunity to cross-sell a more extensive range of products and services to underwriters and insurers with whom they had no prior collaborations, thereby expanding their reach and market presence.

Europe is Growing Steadily in Terms of Insurance TPA

The growing prevalence of chronic diseases, including cancer, diabetes, and heart conditions, can be attributed to the expanding elderly population in the region, leading to a rise in health insurance policies as the demand for healthcare coverage increases in response to the aging demographic.

As per Eurostat, the European Union population was estimated at approximately 448.8 million people in 2023, and over one-fifth (21.3%) of this population was aged 65 years and older. Aging population contributes to the growth of chronic diseases as older adults are more susceptible to chronic conditions such as cancer, diabetes, and heart diseases due to the natural aging process and lifestyle factors.

Moreover, the healthcare expenses in Europe are propelling insurers and employers to outsource administrative tasks to TPAs for cost-effective solutions, driving demand for TPA services in the insurance industry. According to the latest data by Eurostat, in the EU in 2022, health expenditure continued to be the second most significant category of general government spending following 'social protection' expenses. During that year, general governments in the EU allocated USD 1328.2 billion towards health, representing 7.7% of GDP.

Competitive Landscape

The insurance TPA market trends include various market players, such as Sedgwick Claims Management Services Inc., United HealthCare Services (UMR) Inc., Crawford & Co., Gallagher Bassett Services Inc., CorVel Corp., Meritain Health, ESIS Inc., Helmsman Management Services LLC, Trustmark Health Benefits Inc., Cannon Cochran Management Services Inc., dba CCMSI and others. These market players are adopting several strategies such as product launch, collaboration and acquisition across various regions to maintain their dominance in the insurance TPA industry.

For instance, in April 2023, Sedgwick Claims Management Services Inc. recently introduced Sidekick, an artificial intelligence tool designed to enhance workflow for insurance claims professionals.

Moreover, in July 2022, EXL and Xceedance partnered to offer insurers property and casualty claims services, complemented by digital TPA solutions. This collaboration aims to deliver an improved and technologically advanced claims servicing experience to insurers. By combining their expertise, these industry leaders are poised to enhance consumer benefits through the provision of digital TPA services throughout the forecast period.

Also, in April 2022, Gallagher & Co. acquired Claims Settlement Agencies Ltd (CSA) to expand its offerings and expertise, enhancing the experience for both new and existing clients. This strategic acquisition also enables GB to cross-sell additional products and services to underwriters and insurers, contributing to the growth of their business activities.

Additionally, in March 2022, Charles Taylor launched 'InHub,' a cutting-edge solution designed to improve outcomes within the insurance value chain. As a cloud-based SaaS hub, InHub provides a seamless experience for the TPA insurance market and its clients. The introduction of advanced insurance products intensifies competition among industry participants, compelling them to innovate and deliver sophisticated solutions that cater to customer needs and expectations effectively.

Key Market Segments

By Type

-

Health Insurance

-

Diseases Insurance

-

Medical Insurance

-

Senior Citizens

-

Adults

-

Minors

-

-

-

Property and Casualty Insurance

-

Workers' Compensation Insurance

-

Disability Insurance

-

Travel Insurance

-

Others

By Services

-

Claims Management

-

Risk Control Management

By End User

-

Healthcare

-

Construction

-

Real Estate and Hospitality

-

Transportation

-

Staffing

-

Others

By Region

-

North America

-

The U.S.

-

Canada

-

Mexico

-

-

Europe

-

The U.K.

-

Germany

-

France

-

Italy

-

Spain

-

Netherlands

-

Denmark

-

Finland

-

Norway

-

Sweden

-

Russia

-

Rest of Europe

-

-

Asia-Pacific

-

Australia

-

China

-

India

-

Indonesia

-

Japan

-

Singapore

-

South Korea

-

Taiwan

-

Thailand

-

Rest of Asia-Pacific

-

-

RoW

-

Latin America

-

Middle East

-

Africa

-

REPORT SCOPE AND SEGMENTATION:

|

Parameters |

Details |

|

Market Size in 2023 |

USD 350.89 Billion |

|

Revenue Forecast in 2030 |

USD 535.22 Billion |

|

Growth Rate |

CAGR of 4.6% from 2024 to 2030 |

|

Analysis Period |

2023–2030 |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

Market Size Estimation |

Billion (USD) |

|

Growth Factors |

|

|

Countries Covered |

28 |

|

Companies Profiled |

10 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 analysts working hours) after purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

KEY PLAYERS

-

Sedgwick Claims Management Services Inc.

-

United HealthCare Services (UMR) Inc.

-

Crawford & Co.

-

Gallagher Bassett Services Inc.

-

CorVel Corp.

-

Meritain Health

-

ESIS Inc.

-

Helmsman Management Services LLC

-

Trustmark Health Benefits Inc.

-

Cannon Cochran Management Services Inc., dba CCMSI

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

We conduct SWOT analysis to understand market trends, identify potential threats, capitalize on opportunities, and assess our strengths and weaknesses.

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Frequently Asked Questions

Download Free Sample

Related Report

Related Blogs

The Digital Revolution in U.S. Insurance Industry

The U.S. insurance industry is undergoing a significant transformation driven by...

How Leading Players are Adapting to a Rapidly Expanding Insurance TPA Market

The insurance TPA market is experiencing strong growth,...

Adoption of Latest Technologies to Reshape the P&C Core Platform Industry

Introduction The property and casualty (P&C) insurance...

_Insurance.png)