Warehouse Robotics Market by Type (Automated Guided Vehicles (AGVs), Autonomous Mobile Robots (AMRs), Articulated Robots, and Others), by Offering (Hardware, Software, and Services), by Payload Capacity (Less than 100 KG, 101-200 KG, 201-500 KG, and Others), by Application (Palletizing and Depalletizing, Sorting and Packaging, Picking and Placing, Transportation), and by End-User (E-commerce, Automotive, Food & Beverages, and Others)– Global Opportunity Analysis and Industry Forecast 2025–2030

Industry: ICT & Media | Publish Date: 07-Mar-2025 | No of Pages: 966 | No. of Tables: 682 | No. of Figures: 627 | Format: PDF | Report Code : IC424

US Tariff Impact on Warehouse Robotics Market

Trump Tariffs Are Reshaping Global Business

Warehouse Robotics Market Overview

The global Warehouse Robotics Market size was valued at USD 10.11 billion in 2024 and is predicted to reach USD 28.32 billion by 2030 with a CAGR of 17.7% from 2025-2030. In terms of volume the market size was 479.6 thousand units in 2024 and is projected to reach 1466.6 thousand units in 2030, with a CAGR of 19.3% from 2025 to 2030.

Factors such as increased investment in Industry 4.0, rising labor costs alongside workforce shortages and industrial accidents are driving demand for industrial and warehouse robotics.

However, high initial costs and complexity in system integration challenge market growth. On the other hand, collaborative robots (cobots) are achieving success, especially among Small and Medium-sized Enterprises (SMEs) in search of automation solutions.

Key players such as ABB Ltd., Omron Corporation, and others are driving innovation through collaborations and product launches. Thus, the growing adoption of robotics is transforming industrial operations thereby enhancing productivity and addressing workforce challenges.

Growing Investment in Smart Factories and Industry 4.0 Initiatives is Driving the Warehouse Robotics Market Growth

The growth in global investment in Industry 4.0 is contributing to the expansion of the market as these robots are essential to achieve automation, precision, and efficiency in advanced manufacturing and smart factories.

The latest report published by World Economic Forum, 2023, investments in Industry 4.0 initiatives are steadily increasing, where digital transformation is expected to reach USD 298.2 billion in the MENA region up to 2032.

The rising investments in industry 4.0 initiatives are accelerating the adoption of industrial robots, driving significant warehouse robotics market growth by enabling smarter and more efficient manufacturing processes.

Rise in Labour Costs and Workforce Shortages Accelerates the Warehouse Robotics Market Demand

The lack of workers in various countries is compelling the need for robots to be used in warehouses, as these robots can effectively fill labour gaps and maintain productivity in industries that are facing workforce challenges.

According to Conference Board reports of 2024, the U.S. requires 4.6 million new employees every year. Germany, South Korea and China face shortages at a higher scale of 1.6 million, 2 million and 47 million respectively. Such deficiencies force the companies to deploy automation and robots for effective production requirements, thereby contributing to the market growth.

Increased Industrial Accidents Fuel the Requirement for Warehouse Robotics

With a rise in industrial accidents and diseases, the requirement for warehouse robots is increasing since they can undertake hazardous tasks much more safely thereby reducing risk to human workers and improving workplace safety.

According to reports published by International Labour Organisation, in 2023, it is estimated that around 3 million workers die every year from work-related accidents in industries.

This high mortality rate is driving the adoption of warehouse robots that reduce human involvement in hazardous tasks and improve safety in workplaces thereby driving the warehouse robotics market growth.

High Cost and Complexity Associated with the Setup of Warehouse Automation Hinder the Market Growth

High initial investment and the complexity of integrating warehouse automation into existing systems are key challenges hindering the market expansion. The difficulty in affording automation solutions, especially for SMEs, further limits the wider adoption of these solutions. Thus, these issues pose challenges for small enterprise slowing down the adoption of these robots thereby restraining the overall growth of the market.

Growing Adoption of Collaborative Robots is Expected to Create Ample Future Opportunities

Rising demand for cobots in SMEs is highly expected to drive the growth of the market since the cobots can work alongside human workers by mitigating the need for major safety measures. The cobots are also considered cost-efficient as they require minimal setting and easy programming for various purposes.

The latest report from Association for Advancing Automation states, collaborative robots is expected to experience a significant growth over the next several years by reaching USD 7.5 billion by 2027 equating roughly 29% of the overall industrial robots.

Thus, the falling prices combined with their flexibility and ease of integration is anticipated to boost the adoption of cobots that will make automation more accessible for enterprises and thus drive the market growth.

By Type, Articulated Robots Holds the Dominating Share with 31.7% in the Warehouse Robotics Market

Articulated robots dominate the type segment in the warehouse robotics market, holding the largest share with 31.7% share. Their dominance is attributed to their high flexibility, multi-axis movement, and ability to handle complex tasks such as picking, packing, and palletization.

These robots offer enhanced precision and adaptability making them ideal for various warehouse applications from high-speed sorting to heavy-duty lifting. Their seamless integration into automated systems further strengthens their leadership in the market.

By Application, Transportation Holds the Highest CAGR of 19.4%

Transportation will be the most growth-intensive segment, with a projected CAGR of 19.4% during the 2025-2030 period. This growth is primarily driven by the increasing demand for efficient logistics and the need for automation in the transportation sector.

Additionally, advancements in robotics and AI technologies are further boosting the adoption of automated systems, improving speed, accuracy, and cost-effectiveness.

Asia-Pacific Dominates the Warehouse Robotics Market Share

Asia-Pacific, that consists of countries including China, India, Japan, and more holds the highest share in the global warehouse robot market. Investment by the regional governments in subsidies and such initiatives takes a propelling effect on the adoption of industrial robots in the region, driving the growth and expansion of market automation.

As per reports published by ORCA, 2024, China’s government investments in warehouse robots to boosts the market’s growth by increasing the robot density rate to 392 robots per 10,000 workers in 2023, up from 97 in 2017.

China accounted for 52% of global new factory robot installations in 2022, maintaining its position as the largest market. Government investments, therefore, play a key role in boosting warehouse robot adoption as the market continues to experience substantial growth and technological advancement.

Moreover, the increasing number of industrial deaths in the region is pushing up the demand for the warehouse robot market, as companies are seeking automation solutions that will improve the safety of their workers and minimize fatalities.

According to reports released by National Library of Medicines, 2023, South Korea's industrial accident mortality rate is 0.58% that is considerably higher than countries including Germany at 0.16% and the U.S. in 0.36%. This high industrial accident mortality rate in countries is fueling the demand for warehouse robotics to enhance workers safety and reduce fatalities in the region.

North America is Expected to Show a Steady Growth in the Warehouse Robotics Market with a CAGR of 22.8% till 2030

These e-commerce businesses in the regions, such as Amazon, Walmart, and Shopify, are gaining rapid growth across the region at a high order fulfilment rate based on fast delivery, efficiency, and accuracy. As these warehouses grow in the platforms, they need automation solutions such as AMRs, articulated robots, and others to boost their productivity and speed in order fulfilment.

According to the report of the ecommerce tips, the retail ecommerce sales in the U.S. in 2022 were approximately around USD 1.05 trillion, that grew about to USD 1.67 trillion with a CAGR of 12.5%.

Thus, this rising ecommerce sales further emphasize the increased demand for more advanced warehouse robotics to enable companies to operate in a streamlined manner in order to address the surging demands of consumers.

Also, major companies in the country, such as Amazon, DHL, and Walmart, are spending on smart warehouse infrastructure to upscale operational efficiency and scalability. By integration warehouse robots with WMS software and internet of things (IoT), businesses are streamlining management by optimizing workflows, and improving real-time data tracking.

For instance, in October 2023, Amazon introduced new robotics solutions to enhance efficiency and safety across its fulfilment centers. This launch includes Sequoia a robotic system that speeds up inventory management by identifying and moving products quickly, reducing the time needed to process the orders.

Thus, these advancements in smart warehousing and robotics adoption are reshaping the companies by allowing quicker order fulfilment, greater productivity, and higher responsiveness.

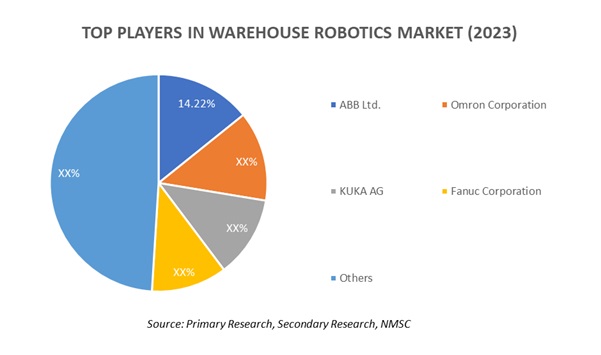

Competitive Landscape

The warehouse robotics industry includes various market players such as ABB Ltd., Omron Corporation, KUKA AG, Fanuc Corporation, JBT Corporation, Teradyne Inc., Geekplus Technology Co., Ltd., GreyOrange, Bastian Solutions, LLC, Locus Robotics, Seegrid Corporation, Doosan Robotics Inc., Lucas Robotics, Zebra Technologies Corporation, Mitsubishi Electric Automation Inc., and others. These market players are adopting several strategies such as product launches, partnerships, and business expansions across various regions to maintain their dominance in the market.

These market players are adopting several strategies such as product launches and partnerships across various regions to maintain their dominance in the market.

|

DATE |

COMPANY |

RECENT DEVELOPMENTS |

|

January 2025 |

Teradyne Inc. |

Teradyne Robotics and Analog Devices partnered on the development of artificial intelligence-driven collaborative automation. The new collaboration incorporates Analog Devices' technology into Teradyne's robotics, further improving performance, safety, and efficiency in many industries, including semiconductor manufacturing. |

|

November 2024 |

FANUC Corporation |

FANUC Corporation announced the introduction of the new five-axis model M-950iA. It is a serial-link articulated robot that operates in confined and restricted work areas. It handles up to 500 kg in payloads. Accordingly, it carries both high-payload capacity along with wide-range motion. |

|

October 2024 |

Mitsubishi Electric Automation Inc. |

Mitsubishi Electric Automation Inc. introduced the MELFA RV-12CRL: a 4.9-foot reach factory robot arm with a maximum lifting capacity of 26 pounds for applications in machine tending, case packing, and pick-and-place operations. |

|

June 2024 |

ABB Ltd. |

ABB Robotics added the IRB 7710 and IRB 7720 to its warehouse robot market portfolio, offering a 25% reduction in cycle times and a 30% decrease in energy consumption. |

|

May 2024 |

Omron Corporation |

OMRON and Neura Robotics collaborated to improve manufacturing efficiency through AI-driven cognitive automation. The OMRON intelligent Cognitive Robot (iCR) series, based on the Neura Robotics MAIRA line, integrates sensors, AI technologies, optional 3D vision, and safety in industrial settings. |

|

January 2024 |

Kuka AG |

KUKA launched KR FORTEC industrial robot, designed for dynamic manipulation tasks featuring high dynamic performance and hence short cycle time at low energy consumption in compact design. The design, with the lines flowing in from all directions, makes this robot suitable for multiple tasks, for example, in automobile production. |

Warehouse Robotics Market Key Segments

By Type

-

Automated Guided Vehicles (AGVs)

-

Laser Guidance

-

Magnetic Guidance

-

Optical Tape Guidance

-

Vision Guidance

-

Others

-

-

Autonomous Mobile Robots (AMRs)

-

Tow Vehicle

-

Tug Vehicle

-

Unit Load Vehicle

-

Pallet Truck

-

Forklift Vehicle

-

Other Type

-

-

Articulated Robots

-

Collaborative Robots

-

Scara Robots and Cylindrical Robots

-

Others

By Offering

-

Hardware

-

Software

-

Warehouse Management System (WMS)

-

Warehouse Execution System (WES)

-

Warehouse Control System (WCS)

-

-

Services

By Payload Capacity

-

Less than 100 KG

-

101-200 KG

-

201-500 KG

-

501-1000 KG

-

1001-2000 KG

-

2001-5000 KG

-

More than 5000 KG

By Application

-

Palletizing and depalletizing

-

Sorting and Packaging

-

Picking and Placing

-

Transportation

By End-User

-

E-commerce

-

Automotive

-

Food & Beverages

-

Pharmaceutical

-

Chemical and Materials

-

Semiconductor and Electronics

-

Others

By Geography

-

North America

-

U.S

-

Canada

-

Mexico

-

-

Europe

-

UK

-

Germany

-

France

-

Italy

-

Spain

-

Denmark

-

Netherlands

-

Finland

-

Sweden

-

Norway

-

Russia

-

Rest of Europe

-

-

Asia-Pacific

-

China

-

Japan

-

India

-

Australia

-

South Korea

-

Taiwan

-

Indonesia

-

Singapore

-

Thailand

-

Rest of Asia-Pacific

-

-

RoW

-

Latin America

-

Middle East

-

Africa

-

Key Players

-

ABB Ltd.

-

Omron Corporation

-

KUKA AG

-

Fanuc Corporation

-

JBT Corporation

-

Teradyne Inc.

-

Geekplus Technology Co., Ltd.

-

GreyOrange

-

Bastian Solutions, LLC

-

Locus Robotics

-

Seegrid Corporation

-

Doosan Robotics Inc.

-

Lucas Robotics

-

Zebra Technologies Corporation

-

Mitsubishi Electric Automation Inc.

REPORT SCOPE AND SEGMENTATION:

|

Parameters |

Details |

|

Market Size in 2024 (Value) |

USD 10.11 Billion |

|

Revenue Forecast in 2030 |

USD 28.32 Billion |

|

Growth Rate (Value) |

CAGR of 17.7% from 2025 to 2030 |

|

Analysis Period |

2024–2030 |

|

Market Volume in 2024 |

USD 479.6 Thousand Unit |

|

Volume Forecast in 2030 |

USD 1466.6 Thousand Unit |

|

Growth Rate (Volume) |

CAGR of 19.3% from 2025 to 2030 |

|

Base Year Considered |

2024 |

|

Forecast Period |

2025–2030 |

|

Market Size Estimation |

Billion (USD) |

|

Growth Factors |

|

|

Countries Covered |

28 |

|

Companies Profiled |

15 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 analysts working hours) after purchase. Addition or alteration to country, regional & segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

We conduct SWOT analysis to understand market trends, identify potential threats, capitalize on opportunities, and assess our strengths and weaknesses.

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Frequently Asked Questions

Download Free Sample

Speak to Our Analyst

Speak to Our Analyst

Related Report

Related Blogs

How Collaborative Robots are Shaping Warehouse Operations

Collaborative robots are used in warehouse operations to revolutionize supply ch...

How Kion, Honeywell, & ABB Lead Warehouse Automation Trends

Next Move Strategy Consulting forecasts that the Warehouse Automation Market wil...

Who’s Leading in Robot Vacuums? Top 10 Innovators Revealed

Next Move Strategy Consulting states that the global robot vacuum cleaner market...