Thailand Aluminium Market by Type (Primary and Secondary), by Product Type (Flat-Rolled, Castings, Extrusions, Forgings, Powder & Paste, Billets, Wire Rods, and Other), By Alloy Series (1xxx Series, 2xxx Series, 3xxx Series, 4xxx Series, 5xxx Series, 6xxx Series, 7xxx Series), by End User (Transportation, Machinery & Equipment, Construction, Packaging, Electrical Engineering, and Other End Users)– Opportunity Analysis and Industry Forecast, 2024–2030

Industry: Materials and Chemical | Publish Date: 23-Apr-2025 | No of Pages: 159 | No. of Tables: 122 | No. of Figures: 67 | Format: PDF | Report Code : MC1408

US Tariff Impact on Thailand Aluminium Market

Trump Tariffs Are Reshaping Global Business

Thailand Aluminium Market Overview

The Thailand Aluminium Market size was valued at USD 5.80 billion in 2023 and is predicted to reach USD 12.19 billion by 2030, with a CAGR of 10.3% from 2024 to 2030.

The aluminum market encompasses the supply and demand dynamics of aluminum, a versatile and lightweight metal extensively used across various industries such as automotive, aerospace, construction, packaging, and electronics. Aluminum plays a crucial role in modern manufacturing and infrastructure development as it is characterized by its properties of corrosion resistance, conductivity, and recyclability.

The market is influenced by factors such as raw material availability, technological advancements in production, economic growth, and environmental regulations. Fluctuations in global trade policies, energy costs, and demand from emerging economies further shape the aluminum market, making it a vital component of the industrial landscape.

Growing Adoption of Aluminum in the Automotive Industry Propels the Thailand Aluminium Market Growth

The automotive industry is a crucial driver of the growing demand for aluminum in Thailand, fueled by an increased focus on light weighting strategies aimed at enhancing fuel efficiency and reducing emissions. Consequently, automotive manufacturers in Thailand are incorporating more aluminum components into their vehicles to meet these goals.

According to data from The Federation of Thai Industries, Thailand's car production has seen a significant rise in recent years. In 2022, the total car production reached 1.88 billion units, with 0.84 billion cars assembled for the domestic market and 1 billion for export. This figure increased to 1.95 billion units in 2023, marking a 3.5% growth from the previous year. Thailand's status as a leading automobile manufacturing hub in Southeast Asia highlights the automotive industry's pivotal role in driving aluminum demand in the country.

Expansion of Electronics Industry Increases Demand for Aluminum Materials Boosts Market Growth

The expansion of Thailand's electronics industry significantly drives the country's aluminum market, with proactive government policies fostering an environment conducive to this industry's development. Thailand's electronics sector has advanced primarily through foreign direct investment (FDI) and trade, with the Board of Investment (BOI) offering incentives and support systems for foreign investors.

This proactive stance, coupled with liberal economic policies and a skilled yet affordable labor force, has made Thailand a key hub for export-oriented production by transnational corporations (TNCs). The electrical and electronics industry, in particular, has garnered substantial interest from American firms.

Notably, recent announcements of significant U.S. investments exceeding USD 1 billion in critical sectors such as solar energy, electric vehicles, and digitization underscore the strong partnership between Thailand and the United States. This influx of investment capital further strengthens Thailand's position as a preferred destination for electronics manufacturing and innovation, boosting demand for aluminum as an essential material in various electronic components and manufacturing processes.

Raw Materials Supply Chain Poses Challenges for the Thailand Aluminium Market

Securing a stable supply of raw materials, particularly bauxite and alumina, is a critical challenge for the aluminum industry in Thailand. The industry relies heavily on imports, exposing Thai producers to various supply chain risks, including geopolitical tensions, trade disruptions, and price volatility, all of which can significantly affect production processes and market dynamics.

Despite Thailand's considerable bauxite reserves, challenges in domestic mining and extraction processes, such as lower-grade ores and environmental concerns, necessitate a substantial reliance on imported raw materials to sustain production levels.

The environmental implications associated with bauxite mining and refining further complicate Thailand's raw material supply chain.

Stringent environmental regulations, including the Environmental Act, BE 2535, and the Minerals Act, along with community opposition to mining activities, pose obstacles to the availability and cost of raw materials. This adds pressure on local aluminum producers to navigate these challenges while ensuring continuity of operations. Overcoming these challenges requires strategic initiatives such as investing in domestic mining and refining capabilities, adopting sustainable practices, and diversifying sourcing channels.

Integration of Artificial Intelligence to Sort Mixed Aluminium Alloy Scrap Creates Market Opportunities

Integration of artificial intelligence (AI) to sort mixed aluminum alloy scrap presents a significant opportunity for the Thailand aluminum market growth. Traditionally, sorting aluminum alloy scrap has been a labor-intensive and time-consuming process, requiring substantial human resources. By employing AI algorithms and machine learning techniques, scrap merchants and smelters in Thailand can streamline the sorting process of mixed aluminum alloy scrap.

These AI systems can quickly and accurately identify different types of aluminum alloys and separate them based on their composition and purity requirements.

This automation not only reduces the time and labor costs associated with manual sorting but also improves the overall efficiency of aluminum recycling operations. By ensuring that only high-quality aluminum scrap is used for recycling, AI-enabled sorting systems contribute to the production of pure aluminum products, meeting the stringent quality standards demanded by various industries.

Moreover, the adoption of AI in sorting aluminum scrap enhances the sustainability of the aluminum industry in Thailand by promoting resource efficiency and reducing waste. By maximizing the utilization of recycled aluminum and minimizing impurities in the manufacturing process, AI-driven sorting technologies contribute to the circular economy and environmental conservation efforts.

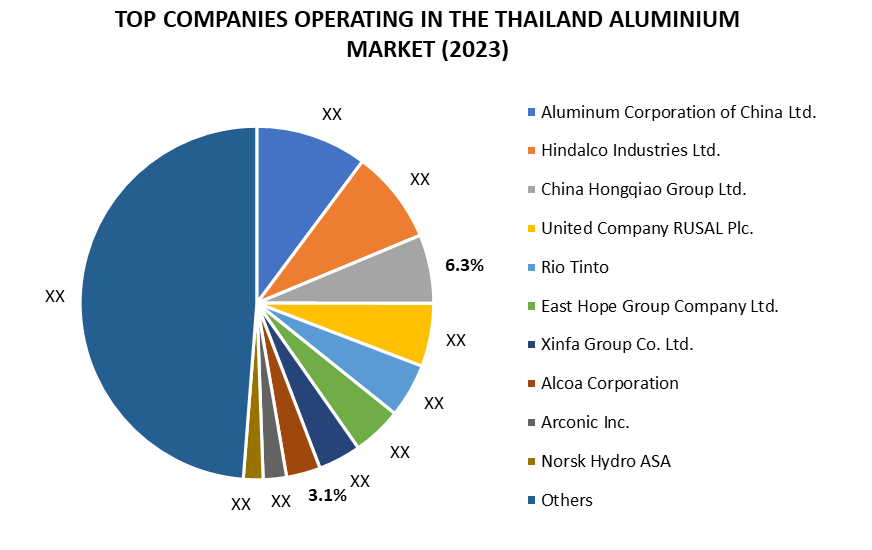

Competitive Landscape

The Thailand aluminium industry comprises various market players, such as Thai Metal Aluminium Co., Ltd., Metalcom Ltd., Varopakorn Public Co., Ltd., Sankyo Tateyama (Thailand) Co., Ltd., Alva Aluminum Ltd., Thai Metal Aluminium Co., Ltd., Metalcom Ltd., Varopakorn Public Co., Ltd., United Aluminium Industry (UAI), Nikkei MC Aluminum (Thailand) Co., Ltd., Aluminum Chue Chin Hua Co., Ltd., ALUCON Public Company Limited, Daiki Aluminium Industry (Thailand) Co., Ltd., TOYAL(THAILAND)Co., Ltd., Henan Mingtai Aluminum Co., Ltd, and others.

Source: Primary Research, Secondary Research, Next Move Strategy Consulting

Source: Primary Research, Secondary Research, Next Move Strategy Consulting

These market players are adopting various strategies including product launches across various regions to maintain their dominance in Thailand aluminium market. By continuously innovating and launching new offerings, they aim to meet the evolving demands of customers and also enables them to capture new opportunities and expand their market share.

|

DATE |

COMPANY |

RECENT DEVELOPMENTS |

|

|

August 2023 |

Hindalco |

Hindalco partnered with Texmaco to manufacture aluminium rail wagons and coaches. The strategic alliance underscores the role of aluminium in modernizing rail transport and reducing its carbon footprint, showcasing the aluminium market's contribution to enhancing sustainable transportation solutions. |

|

|

July 2023 |

Rio Tinto and Giampaolo Group |

Rio Tinto partnered with Giampaolo Group to establish a joint venture focused on aluminium recycling. The collaboration aims to create a more sustainable approach to aluminium production by leveraging Matalco Inc., a renowned aluminium recycling specialist. This strategic partnership is set to boost aluminium recycling capabilities, fostering innovation and contributing to a greener future for the aluminium industry. |

|

|

June 2023 |

Arconic Inc. |

Arconic Inc collaborated with the U.S. Department of Defense (DoD) to expand domestic manufacturing, aiming to bolster the nation's missile capabilities. The collaboration between the DoD and Arconic underscores the critical role of aluminium and other materials in producing high-quality missile components, showcasing the integral connection between aluminium market dynamics and national security interests. |

|

|

May 2023 |

Alcoa and Emirates Global Aluminium (EGA) |

Alcoa and Emirates Global Aluminium (EGA) signed a long-term agreement for the supply of alumina. This strategic collaboration supports the growth and stability of the aluminium market, ensuring a reliable source of alumina for EGA's aluminium smelters and reinforcing Alcoa's position as a leading global supplier in the industry. |

|

|

July 2022 |

China Hongqiao Group Limited |

China Hongqiao Group Limited announced comprehensive roadmap to achieve carbon neutrality by 2055. This ambitious plan includes measures to reduce carbon emissions across its operations and transition towards sustainable practices. The company's commitment to achieving carbon neutrality aligns with the global trend of sustainability in the aluminium market. |

|

Thailand Aluminium Market Key Segments

By Type

-

Primary

-

Secondary

By Product Type

-

Flat-Rolled

-

Castings

-

Extrusions

-

Forgings

-

Powder & Paste

-

Other Types

By Alloy Series

-

1xxx Series

-

2xxx Series

-

3xxx Series

-

4xxx Series

-

5xxx Series

-

6xxx Series

-

7xxx Series

By End User Industry

-

Transport

-

Aerospace

-

Automotive

-

Marine

-

-

Consumer Goods

-

Machinery & Equipment

-

Construction

-

Packaging

-

Food & Beverage

-

Cosmetics

-

Others

-

-

Electrical Engineering

-

Others

Key Players

-

Thai Metal Aluminium Co., Ltd.

-

Metalcom Ltd.

-

Varopakorn Public Co., Ltd.

-

Sankyo Tateyama (Thailand) Co., Ltd.

-

Alva Aluminum Ltd.

-

Thai Metal Aluminium Co., Ltd.

-

Metalcom Ltd.

-

Varopakorn Public Co., Ltd.

-

United Aluminium Industry (UAI)

-

Nikkei MC Aluminum (Thailand) Co., Ltd.

-

Aluminum Chue Chin Hua Co., Ltd.

-

ALUCON Public Company Limited

-

Daiki Aluminium Industry (Thailand) Co., Ltd.

-

TOYAL(THAILAND)Co., Ltd.

-

Henan Mingtai Aluminum Co., Ltd

Report Scope and Segmentation:

|

Parameters |

Details |

|

Market Size in 2023 |

USD 5.80 Billion |

|

Revenue Forecast in 2030 |

USD 12.19 Billion |

|

Growth Rate |

CAGR of 10.3% from 2024 to 2030 |

|

Analysis Period |

2023–2030 |

|

Base Year Considered |

2023 |

|

Forecast Period |

2024–2030 |

|

Market Size Estimation |

Billion (USD) |

|

Growth Factors |

|

|

Companies Profiled |

15 |

|

Market Share |

Available for 10 companies |

|

Customization Scope |

Free customization (equivalent up to 80 working hours of analysts) after purchase. Addition or alteration to country, regional, and segment scope. |

|

Pricing and Purchase Options |

Avail customized purchase options to meet your exact research needs. |

At Next Move Strategy Consulting, we understand that insightful market research is the cornerstone of successful business decisions. That's why we employ a robust and multifaceted approach, combining various methodologies to deliver the most accurate and actionable data for our clients.

Research Landscape

We navigate the world of research with two primary approaches:

Qualitative Approach

Our qualitative research methodologies involve immersive techniques such as in-depth interviews, focus groups, and observational studies. By engaging directly with individuals and stakeholders, we uncover valuable insights that quantitative data alone may overlook.

Quantitative Research

In tandem with qualitative methodologies, NMSC leverages the power of Quantitative Research to provide a robust foundation of numerical insights. Through systematic data collection and analysis, we quantify patterns, preferences, and market trends, offering a comprehensive view of the business landscape.

Our quantitative research approach employs diverse tools, including surveys, experiments, and statistical modelling. These methodologies enable us to gather data from a large and representative sample, ensuring the statistical significance of our findings. By employing structured questionnaires and standardized data collection methods, we guarantee the reliability and validity of the information we present to our clients.

Quantitative research is particularly effective in measuring the prevalence of trends, assessing market size, and gauging the impact of various factors on consumer behavior. The numerical precision attained through this approach equips our clients with actionable insights, facilitating data-driven decision-making and strategy formulation.

Our Specialized Toolbox for Industry-Specific Market Research

We deploy a specialized arsenal of techniques tailored to meet your unique requirements. Here's a glimpse into our comprehensive toolbox:

Information Procurement

The stage entails acquiring market data or relevant information through various sources and methodologies.

Market Research Approach

We utilize both top-down and bottom-up approaches in market research analysis to achieve a comprehensive understanding of the market dynamics, leveraging the broad perspective of industry trends and macroeconomic factors alongside detailed insights from specific segments and individual companies.

Porters Five Forces Analysis

We conduct Porter's Five Forces analysis to evaluate the competitive landscape of an industry, providing us with insights into factors that affect profitability and strategic positioning.

SWOT Analysis

We conduct SWOT analysis to understand market trends, identify potential threats, capitalize on opportunities, and assess our strengths and weaknesses.

Forecasting

We utilize a forecasting model to predict future consumption by considering parameters like population, economics, regulations, market competition, drivers, constraints, technology, and pricing. We also employ statistical techniques such as multilinear regression, exponential smoothing, moving average, ARIMA, and Monte Carlo simulations for accurate predictions. In econometric forecasting, we analyzed short-term and long-term event impacts, attributing values based on regulatory frameworks, economic factors, and market events.

Frequently Asked Questions

Download Free Sample

Speak to Our Analyst

Speak to Our Analyst

Related Blogs

Top Companies Shaping The Future Of Aluminium Production And Supply

The aluminium sector is expected to see a mind-boggling grow...

Impact of Green Policies and Carbon Regulations on Aluminum Market

The aluminium market is undergoing significant transfor...

Cold Pipe Insulation Market: Why Giants Hold 70% Share

Next Move Strategy Consulting forecasts a notable upsurge in the Cold Pipe Insul...